May 25, 2011

As explained previously in this blog a key indicator the Civic Federation uses to assess the financial health of local governments is the level of unreserved general fund balance maintained. Such reserves are essential in order for the governments to be able to withstand the inevitable “rainy days” that result from revenue fluctuations and unexpected expenditures. Without a fund balance in place, a government may have to abruptly cut services or raise taxes in response to unfavorable conditions.

The Civic Federation believes that a critical step toward maintaining a healthy fund balance is to set a clear target through a formal fund balance policy that is adopted by the governing body and included in the budget. Adoption of such a policy can also be important for long-range financial planning. The Government Finance Officers Association (GFOA) also recommends that governments adopt a fund balance policy so they will have a framework to determine whether to increase or decrease the level of fund balance.[1] While GFOA recommends that governments maintain a balance equivalent to two months of operating revenues or expenditures, it also notes that in practice a smaller balance may be appropriate for the largest governments and that all governments should consider their unique circumstances when developing a policy.

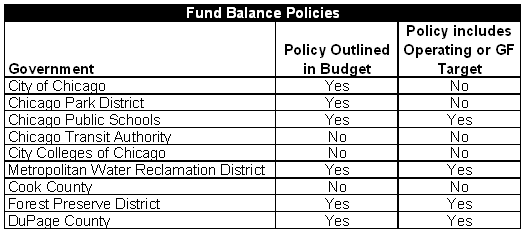

The Civic Federation annually analyzes the budgets of nine Chicago area local governments. Of those, six governments had a fund balance policy outlined in their FY2011 budget while three had no policy. However, only four governments included a specific fund balance target for their general fund or operating funds.

The following is a summary of the fund balance policies:

- City of Chicago: The City’s budget includes a policy regarding financial reserves. However, it only states that the City has established a $500.0 million long-term reserve from the lease of the Chicago Skyway[2] and that operating reserves in its enterprise funds are established to pay for unforeseen emergencies or shortfalls caused by revenue declines.[3] It does not address the City’s corporate fund.

- Chicago Park District: Like the City of Chicago, the Park District has a policy regarding its reserve fund that does not address its general fund. The reserve is available due to the transfer of several public parking structures to the City of Chicago in 2006.[4] The District’s policy establishes a floor of $85.0 million for its reserve fund and allows for internal lending to the general fund in order to bridge timing gaps in property tax collections.[5]

- Chicago Public Schools: The CPSpolicy notes that its goals are to maintain an adequate fund balance to provide working capital, to ensure uninterrupted services, to provide for capital improvements and to achieve a balanced budget within a four-year period. The policy requires CPS to maintain an unreserved fund balance in the operating and debt funds of 5% to 10% of the budget for each new fiscal year. It adds that once that stabilization is adequately established, any excess fund balance can be appropriated under certain circumstances, including to offset a temporary reduction in revenues from local, state and federal sources.[6]

- Metropolitan Water Reclamation District: MWRD develops its budget with the goal of maintaining an unreserved corporate fund balance of $45 to $55 million.[7] Beginning in 2004, the District began to set aside a portion of the net assets appropriable as a non-appropriated or unreserved fund balance that would be available for contingencies.[8]

- Forest Preserve District of Cook County: The District’s policy on unreserved fund balance requires it to annually budget a minimum unreserved fund balance totaling the sum of: 5.5% of corporate fund gross revenues to account for revenue fluctuations; 1% of corporate fund expenditures to account for unexpected expenditures; and 8% of corporate fund expenditures to account for insufficient operating cash.

- DuPage County: The DuPage County financial policies include a goal to maintain a general fund cash balance of between 20-25% of total expenditures plus transfers out. It is designed to accommodate revenue and expenditure cash flow while providing a low point operating margin of one-month’s normal operations.[9]

The City of Chicago and Park District policies are insufficient because they only address reserves from lease proceeds and do not include the general fund. The lease reserves provide the governments with additional liquidity and therefore a lower fund balance target may be appropriate, but they are not a substitute for a general fund balance. The Civic Federation recommended in its Cook County Modernization Report that Cook County adopt financial policies, including a fund balance policy, which the administration supports but has not implemented. CPS and the Forest Preserve District have the most detailed policies of the governments reviewed; both policies clearly outline a numeric goal as well as the reasoning for that target.

In its review of local government budgets, the Civic Federation focuses on whether the government has adopted a policy with a reasonable target and whether it is making progress towards that goal. The Civic Federation also recognizes that it may be appropriate to utilize some fund balance during an economic downturn, which may temporarily place the government below its target. This is why the Civic Federation recommends that adopted policies also outline the circumstances under which a drawdown of balances is appropriate.