November 28, 2012

The Chicago Park District recently released its $410.9 million spending plan for FY2013. The District had identified a $16.0 million budget gap, which it proposes to close with district-wide shut-down days, position eliminations, refinancing debt and some revenue enhancements. In addition, the District plans to use approximately $10.7 million in General Fund fund balance and prior year resources. This comes after the District planned to use $17.2 million in General Fund fund balance last year and $3.0 million in FY2011.

Though the District maintains a healthy level of reserves, the continued use of one-time revenue sources to cover its operating expenses could be an indicator of fiscal stress and should be monitored. This blog is the first of a two-part series discussing the District’s General Fund fund balance levels from FY2006 to FY2011, the most recent years for which audited data are available. The Civic Federation plans to release its full analysis of the Park District’s FY2013 proposed budget next week.

Fund Balance

Fund balance is commonly used to describe the net assets of a governmental fund and serves as a measure of financial resources.[1] It is an important financial indicator for local governments. Fund balance is more a measure of liquidity than of net worth and can be thought of as the savings account of the local government.[2]

This blog discusses three aspects of fund balance: the recent changes to fund balance reporting with the implementation of the Governmental Accounting Standards Board Statement No. 54, a presentation of the Chicago Park District’s General Fund fund balance and the fund balance for funds the District created with proceeds from the intergovernmental sale of its parking garages.

Recent Changes to Fund Balance Reporting

The FY2011 audited financial statements for the Chicago Park District include modifications in fund balance reporting, as recommended by the Governmental Accounting Standards Board (GASB). GASB Statement No. 54 shifts the focus of fund balance reporting from the availability of fund resources for budgeting purposes to the “extent to which the government is bound to honor constraints on the specific purposes for which amounts in the fund can be spent.”[3] A detailed explanation of previous components and new components of fund balance can be found in this previous blog.

In addition to the reporting changes, GASB 54 clarified the definition for governmental fund types. As a result, the Chicago Park District merged the Long-Term Income Reserve and Northerly Island funds with the General Fund since they no longer met the definition of a special revenue fund. The Long-Term Income Reserve was available due to the sale of several public parking structures to the City of Chicago in 2006.[4] Interest earnings from the fund were intended to replace the revenue that was formerly generated through parking garage revenues. The District had a policy in place to maintain a balance in its Long-Term Income Reserve Fund. The District’s policy established a floor of $85.0 million for the Long-Term Income Reserve Fund and allowed for internal lending to the General Fund in order to bridge timing gaps in property tax collections.[5] With the implementation of GASB 54, the balance of the Long-Term Income Reserve fund was merged into the General Fund.

Historically, the focus of the Civic Federation fund balance analysis has been on the unreserved general fund balance, or in other words, how much is left in the savings account, not how much is being withdrawn. Given the new components of fund balance established by GASB Statement No. 54, the Civic Federation now focuses on a government’s unrestricted fund balance, which includes the committed, assigned and unassigned fund balance levels. The only difference between the two terms (unreserved and unrestricted) is that a portion of what used to be categorized as unreserved fund balance is now reported as restricted fund balance; otherwise, the two terms are nearly synonymous.[6]

A five-year trend analysis of the District’s fund balance ratio including the most recent FY2011 numbers is not possible because the data has been classified differently with implementation of GASB No. 54. In the interest of government transparency, the Civic Federation recommends that all local governments, if possible, provide ten years of fiscal data in the GASB No. 54 format in the statistical section of their audited financial statements. Each government should also provide a guide as to how different fund balance lines were reclassified. An accurate trend analysis can only be conducted with reclassified data.

Fund Balance for the General Fund

The Government Finance Officers Association (GFOA) recommends “at a minimum, that general-purpose governments, regardless of size, maintain unrestricted fund balance in their general fund of no less than two months of regular general fund operating revenues or regular general fund operating expenditures.” Two months of operating expenditures is approximately 17%.[7] In 2012 the Park District established a General Fund fund balance policy to maintain at least $25.0 million in the General Fund. This represents 6.1% of the proposed FY2013 operating expenditures of $410.9 million. The Civic Federation supported this initiative but also encourages the District to implement a fund balance policy according to guidelines recommended by the GFOA.

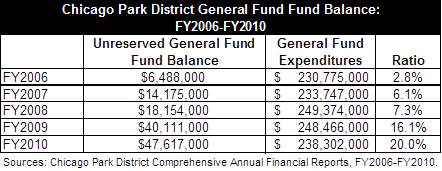

From FY2006 to FY2010, the General Fund fund balance fluctuated considerably between a low of 2.8% in FY2006 and a high of 20.0% in FY2010. The Chicago Park District attributes the $22.0 million increase in the General Fund fund balance in FY2009 from FY2008 to a $10.6 million transfer of fund balance from the Public Building Commission (PBC) Operating Fund, a $7.9 million transfer from the Garage Revenue Capital Improvements Fund, $2.1 million transfer from the Long Term Income Reserve Fund and revenues exceeding expenditures.[8] In FY2010 the General Fund fund balance reached $47.6 million, or 20.0% of operating expenditures, thereby exceeding the GFOA’s fund balance recommendations.

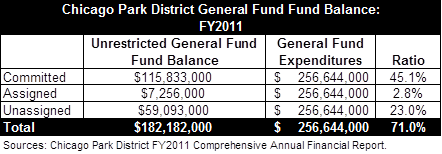

In FY2011 the District’s unrestricted General Fund fund balance was $182.2 million, or approximately 71.0% of General Fund expenditures. According to the audited financial statement and as noted above, the unrestricted fund balance includes $95.8 million related to the Long-Term Income Reserve Fund and $4.3 million related to the Northerly Island Fund, which were previously reported separately as special revenue funds.[9]

Next week, the Civic Federation will continue this blog series with an analysis of the reserve funds created with proceeds from the intergovernmental sale of the District’s parking garages.

[1] Government Finance Officers Association, Appropriate Level of Unrestricted Fund Balance in the General Fund (Adopted October 2009).

[2] Stephen J. Gauthier, The New Fund Balance (Chicago: GFOA, 2009), p. 34.

[3] Gauthier, Stephen J., “Fund Balance: New and Improved,” Government Finance Review, April 2009 and GASB Statement No. 54, paragraph 5.

[4] Chicago Park District FY2009 Comprehensive Annual Financial Report, p. 50.

[5] Chicago Park District FY2009 Comprehensive Annual Financial Report, p. 30.

[6] Gauthier, Stephen J., The New Fund Balance (Chicago: GFOA, 2009), p. 34.

[7] Previously the GFOA had recommended a General Fund fund balance of 5 to 15%.

[8] Chicago Park District FY2011 Budget Summary, pp. 15 and 36.

[9] Chicago Park District FY2011 Comprehensive Annual Financial Report, p. 17.