November 05, 2010

After experiencing several years of poor market conditions, three of the five Illinois State employee retirement funds have reduced their expected rate of return on investments. This rate, also known as the discount rate, is used to calculate the present value of the future obligations of the systems. Although the reductions were small, one percentage point or less, the move triggers a substantial increase in the present value of the commitments made by the State to its employees and retirees. The increase in liabilities will also trigger an increase in the required annual contribution the State will pay into the systems starting in FY2012, further straining the already beleaguered State budget.

According to the Chicago Tribune, the largest of the retirement funds, the Teachers Retirement System (TRS), and the smallest, the General Assembly Retirement System, have so far refrained from changing their assumed rate of return. However, the State Universities Retirement System (SURS), State Employees' Retirement System (SERS), and Judges' Retirement System (JRS), whose members collectively make up nearly half of the more than 300,000 total active retirement system participants, will reduce the assumed rate of return thus increasing the unfunded liabilities calculated for these systems.

Previously, all five of the state employees’ retirement systems used an estimated annual rate of return of 8.0 % or 8.5% when computing the present value of the unfunded liabilities of the pension funds. Two of the three largest funds, SURS and SERS, each reduced the discount rates from 8.5% to 7.75%. The judicial employees fund will now use 7% rather than 8%.

The discount rate has an inverse relationship to actuarial liabilities such that a lower discount rate will result in higher liabilities. A high assumed rate of return may be attractive because it minimizes liabilities but it should remain realistic.

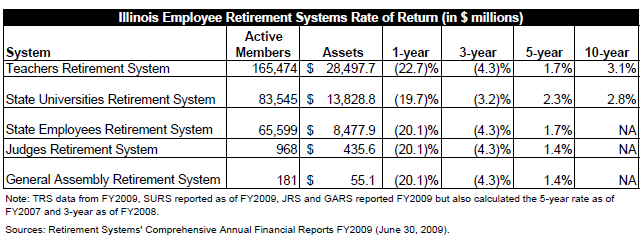

According to the most recent Comprehensive Annual Financial Reports, even the actual five -year and 10-year returns for the funds have been well below 8%.

Although the retirement systems have provided some monthly and quarterly updates since the last annual reports, so far only TRS has published updated annual investment results for FY2010. It appears that the teachers’ system may be waiting to alter its estimated rate of return due to significant investment gains in the past fiscal year. TRS reported a 13.5% rate of return in the fiscal year ending June 30, 2010. The following chart shows the updated investment data provided by TRS.

Officials from TRS also have said that the fund has reported a 25-year rate of return of 8.6%, slightly beating the target rate used to calculate the present value of its unfunded liabilities.

According to the Chicago Tribune article, the change in the rate for the SURS fund will increase its unfunded liability by 8%, or $2.4 billion. SURS officials said the increase in liability will lead to nearly a $100 million increase in the FY2012 State pension payment. This is nearly a 10% increase in the SURS portion of the annual State contribution. Estimates of the effect of the rate change for the other funds are not yet available.

The increases in annual payments required from the State resulting from the lower discount rates could also offset much of the expected savings from pension reforms passed earlier this year. The State enacted SB1946 on April 14, 2010, which reduced pension benefits for employees hired after January 1, 2011, thus reducing the anticipated growth in the unfunded liabilities for future employees. It did not however apply to any current employees so the current total unfunded pension liability of approximately $62.4 billion was not affected by the law.

The State’s FY2011 payment was certified earlier in the year and is based on FY2010 calculations, so the increase in the unfunded liabilities due to the reduced discount rate would not increase the State’s payment until FY2012. However, the State already cannot afford its current required annual payment.

Legislation is still under consideration in the Illinois Senate to borrow in order to make the State’s $4.1 billion FY2011 pension payment due to a lack of operating funds. Although the pension borrowing bill, SB3514, passed the House of Representatives on May 25, 2010, the Senate has yet to vote on the plan. If approved it would be the third time the State sold Pension Obligations Bonds (POBs) in the last ten years and total pension related debt would total more than $17 billion.

The Senate began deliberations on the bill on November 4, 2010, in the Executive Committee but the matter was tabled until the General Assembly’s veto session begins on November 16, 2010.

Borrowing to make its annual pension payment adds an additional layer of interest to the State’s annual pension costs and increases the strain from pensions on future budgets by pushing forward current liabilities. As previously discussed on this blog, debt service due on pension borrowing increased from $543.3 million in FY2010 to more than $1.3 billion in FY2011. Including other transfers related to this debt, the current budget plan estimated a combined FY2011 cost of more than $1.7 billion. In order to cope with the additional debt cost that would come with borrowing for pensions in FY2011, the State plans to backload the new bonds over the next eight years. This means it will not pay down principal on the new bonds until after the FY2010 bonds are paid off in FY2015. The back-loaded structure will lead to much higher interest for the proposed FY2011 pension bonds, which could total as much as $1 billion depending on the final terms of the bond sale.