November 25, 2015

In the absence of a budget for FY2016, the State of Illinois is moving forward with a plan to issue debt through the Illinois Finance Authority to fund some essential operating expenses.

However, the loans could cost the State millions in interest over the next 10 to 20 years based on information being circulated by the IFA to potential underwriters for the bonds.

According to procurement documents on the IFA website, the Authority currently has statutory approval to issue $115 million in moral obligation debt. These funds then could be loaned to local governments and service providers to pay for operations that usually would be funded through State appropriations but that have not yet been enacted for FY2016.

The IFA already withdrew $12 million of its existing fund balance totaling $17 million to provide similar funding to local governments for 911 services, snow plow repairs and other essential services. Although these loans are being provided by the IFA without any interest or fees, the moral obligation loans will be more costly.

A moral obligation bond differs from a General Obligation bond (GO Bond) because it is only backed by the pledge of a future appropriation from the State, not the full faith and credit. The repayment of GO Bonds are automatically funded every year by a continuing appropriation. This protects bond holders from missing any payments due to budgetary issues such as a revenue shortfall or the sort of budget impasse that the State is currently experiencing.

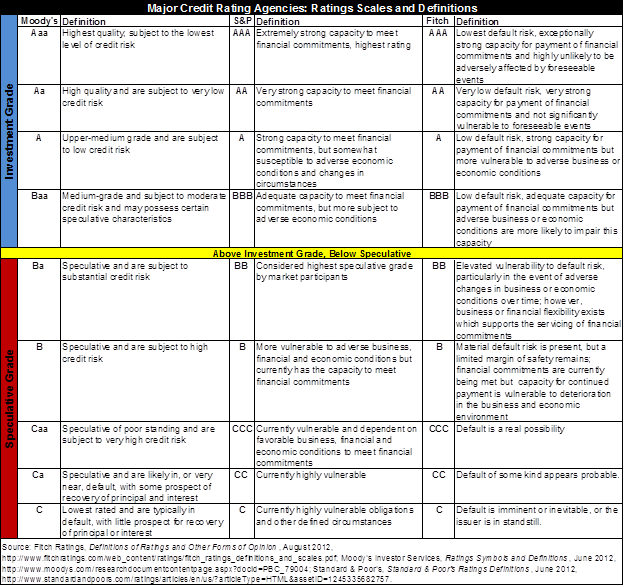

Investors take on more risk when buying a moral obligation bond. They are typically rated an entire grade level lower than GO Bonds and garner much higher interest rates.

The State of Illinois is currently rated on the BBB+ by Fitch and Baa1 by Moody’s Investors Service. So any moral obligation bonds issued by the IFA would likely be rated on the BB level, which is below investment grade.

{kind=link}

Under the Illinois Financial Authority Act, the Governor is required to notify the General Assembly of any moral obligation bond debt service not payable within the Authority’s current budget prior to the end of the current fiscal year. However, the statute does not force the General Assembly to approve the requested funds.

State statute currently allows for $150 million of moral obligation debt to be outstanding at any time. The IFA currently manages $35 million outstanding State moral obligation debt and makes debt service payments as part of its annual budget. In response to questions submitted to the IFA from potential lenders, the Governor intends to include a line-item appropriation in the FY2017 budget to make a debt service payment on the new loan. Documents also instruct investors to propose loans structured for between 10 to 20 years.

By using this existing bonding authority under the Illinois Finance Authority Act, the Governor will be able to provide State funding without the need for appropriation authority from the General Assembly. However, the current State operations funded with this debt will increase the total cost of providing government services by the interest and fees related to issuing the moral obligation bonds and extend the costs into future fiscal years.

The specific State expenditures that could be funded by the moral obligation bonds have not been publicized by the Governor’s Office of Management and Budget (GOMB). However, background materials on the plan stated the following criterial must be met to qualify for the loans:

- The goods or services are essential for the State’s ongoing, core operations, such that interruption of the provision of those goods or services would (i) pose a threat to public health or public safety, (ii) disrupt State services that affect public health or public safety or the collection of substantial State revenues, (iii) prevent the State from repairing property in order to protect against further loss or damage to State property, or (iv) prevent the State from ensuring the integrity of its records. The determination of whether goods or services meet these criteria will be made by GOMB, the Department of Central Management Services, and the State agency that procured or received the goods or services;

- Payment for the goods or services would be authorized by both (i) the Fiscal Year 2016 budget proposed by the Governor and (ii) the Fiscal Year 2016 appropriation bills passed by the General Assembly. This is intended to demonstrate that neither the Governor nor the General Assembly has proposed terminating funding for these goods or services;

- The goods or services have been provided to the State, as documented by the following: (i) there is a valid contract between the vendor and the State for the provision of the goods or services; (ii) the vendor has provided an invoice to the State for the goods or services; and (iii) the agency has provided an acknowledgement that the goods or services were received by the State; and

- The State has consistently and historically funded payment for the goods or services in prior fiscal years. The State agency that is responsible for processing the invoice will provide documentation of prior payments by the State for the goods or services.