September 01, 2011

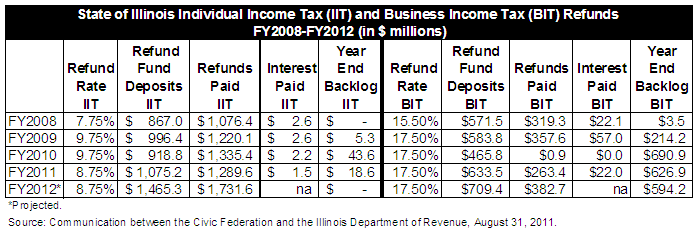

The State of Illinois still owes income tax refunds to many businesses, but the backlog declined in the fiscal year ended June 30, 2011 and is expected to dip further this year.

According to the Illinois Department of Revenue, 4,569 businesses were owed $626.9 million in income tax refunds at the end of FY2011, down from $690.9 million at the end of FY2010. Nearly 34,000 individuals were owed $18.6 million at the end of FY2011, down from $43.6 million at the end of FY2010, but all of the individual tax refunds were paid by early July 2011.

By the end of FY2012, the Revenue Department expects the backlog of business refunds to decrease slightly to $594.2 million, while refunds owed to individuals are expected to be fully paid.

As previously discussed here and shown in the table below, the backlog of approved but unpaid business income tax refunds had been growing since FY2009. The State paid less than $1 million in business refunds in FY2010 compared with $263.4 million in FY2011.

In April 2011, the Revenue Department had estimated that the backlog of business refunds would reach roughly $879 million by the end of FY2011, but it reached only $626.9 million. Officials attributed the reduction to a change in business practices after the past few years of delayed refunds. More businesses applied refunds owed to the next year’s tax bills or estimated their tax obligations more conservatively to prevent overpayments.

Unlike unpaid bills to vendors and local governments, unpaid tax refunds are not reflected in the State’s operating budget plan. To pay income tax refunds owed to taxpayers, the State sets aside a percentage of income tax receipts received throughout the year and deposits them into a special fund. Different percentages apply to individuals and businesses, but all refunds are paid from the same fund—the Income Tax Refund Fund.

The percentages are known as Refund Fund rates. The higher the Refund Fund rates, the more money deposited into the fund and the less revenue available for the State’s general operations. A higher rate also reduces the share of income taxes transferred to local governments. The Illinois Department of Revenue makes it a priority to pay personal income tax refunds to individuals, so when there is a shortfall in the fund, unpaid business refunds rise.

The Refund Fund rate for businesses covers both the income tax and the Personal Property Replacement Tax (PPRT) on corporations and the PPRT on subchapter S corporations, partnerships and estates. Replacement taxes are revenues collected by the State and paid to local governments to replace money that was lost by local governments when their power to impose personal property taxes on corporations, partnerships and other business entities was rescinded pursuant to the 1970 Illinois Constitution.

As explained here, Refund Fund rates are set by the Illinois General Assembly or can be set through a statutory formula that takes into account both refunds paid and refunds approved but unpaid from the prior year as well as income tax revenues from the prior year. The last time the rate was set using the formula was FY1998. Since then it has been specifically designated in budget legislation passed by the General Assembly and signed by the Governor.

Despite the backlog of corporate refunds, the State lowered the Refund Fund rate for individual income taxes from 9.75% in FY2010 to 8.75% in FY2011 and kept the rate unchanged for FY2012. The business refund rate has been held constant at 17.5%. Governor Pat Quinn had proposed lowering the business refund rate to 12.5% in FY2012 and paying down the refund backlog through borrowing, but the General Assembly did not approve the proposal.

The table above also shows interest payments on unpaid refunds, although projections are not available for FY2012. The state currently pays interest at 1% a year for the first year and 4% thereafter.