March 12, 2026

by Paula R. Worthington

Download the Executive Summary

Last week’s employment report confirmed weakness in recent job growth nationwide, with preliminary data pointing to a 92,000 decline in nonfarm employment in February 2026. The national unemployment rate also ticked up slightly to 4.4%. While one month of data is not definitive, the basic picture appears to be one of a labor market “treading water,” creating just enough jobs to keep the unemployment rate from rising too sharply.

Closer to home, available data and forecasts also point to a weakening job market in the State of Illinois (Illinois or ‘the State’). Moody’s recent report highlights last year’s manufacturing sector weakness alongside the healthcare sector’s strength and points to 2026 “drags” on employment and economic activity coming from uncertainty about trade policy. Adding the volatility from international conflicts only makes the 2026 prospects less certain.

In fact, last week’s spike in oil prices reminds us of how conflict in the Middle East can affect economic activity in the U.S. A sustained increase in oil prices pushes up energy costs, affecting energy-intensive sectors such as manufacturing and transportation. One rule of thumb is that each $10 increase in the crude price per barrel is associated with a 0.1 percentage-point increase in inflation and a 0.1 percentage-point decrease in GDP growth—that is, a worsening of both inflation and growth. On balance, pressures from prolonged conflict and elevated oil prices could lead to declines in economically sensitive revenues such as income and sales taxes in states across the country.

As the Illinois General Assembly takes up Governor Pritzker’s budget proposal, getting a realistic picture of the current state of labor markets is essential as FY2027 approaches. In this report, we discuss both national and state labor market conditions, highlighting key sectors and the risks likely to matter most in the months ahead.

US Job Growth Has Stalled

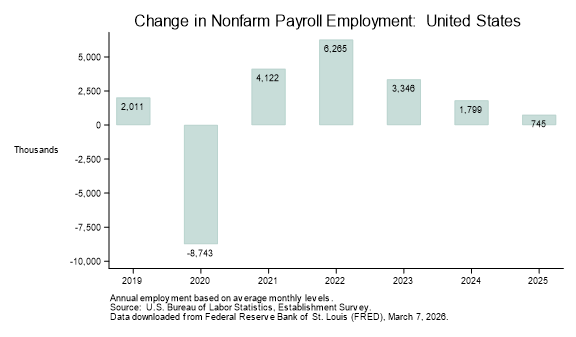

On an annual basis, job growth in 2025 declined, with employers adding just 745,000 jobs, the lowest level post-COVID:

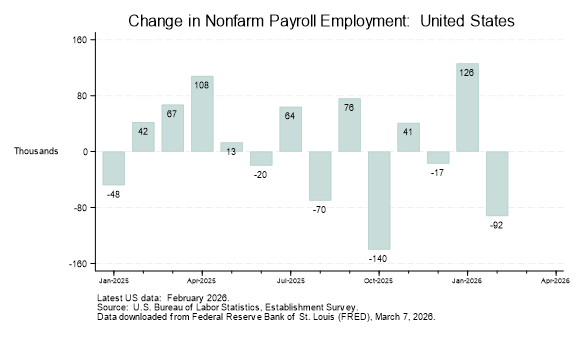

Monthly data on job growth from 2025 onward has been erratic and uneven, with January 2026’s burst (up 126,000) followed by February’s decline (down 92,000).

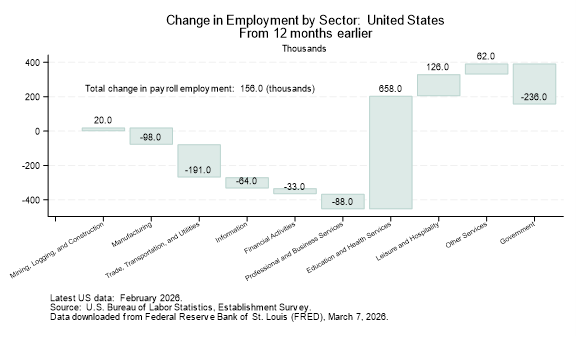

Over the past 12 months, payrolls are up only 156,000—implying an average monthly change of only 13,000--with strength in the education and health services sector outweighing weaknesses elsewhere. Despite this anemic job growth, the unemployment rate has ticked up only slightly, from 4.2% in February 2025 to 4.4% in February 2026. Why the disconnect between essentially steady unemployment rates and very weak job growth? The labor force has stopped growing—indeed, by some measures, it has declined. In a nutshell, far fewer new jobs are needed each month to keep the unemployment rate essentially unchanged.

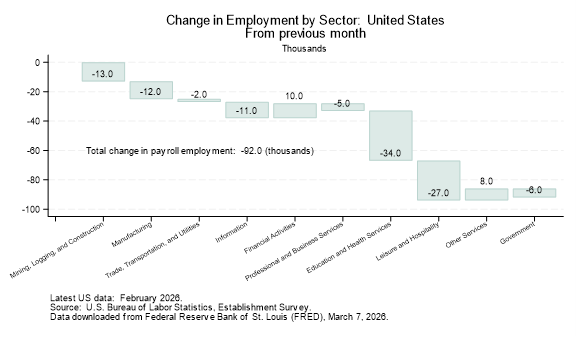

February’s loss of 92,000 jobs was widespread across sectors and included declines in both the education and health services sector and the leisure and hospitality sector, both of which contributed significantly to job growth last year.

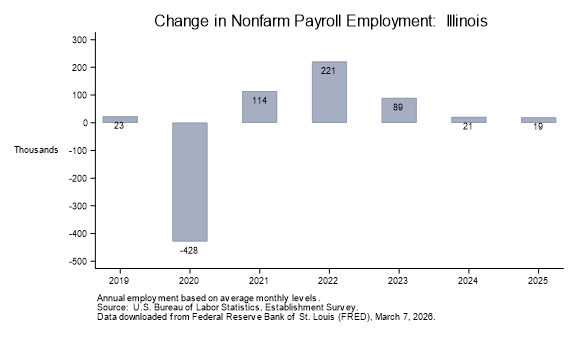

Illinois: Same or Different?

As we have previously noted, Illinois’s post-COVID recovery was weaker than that of the nation as a whole. That said, as seen in the chart below, 2025 played out for Illinois similarly to the U.S. overall: fairly anemic. Employment rose in the State by only 19,000, little changed from 2024’s gain of 21,000 jobs.

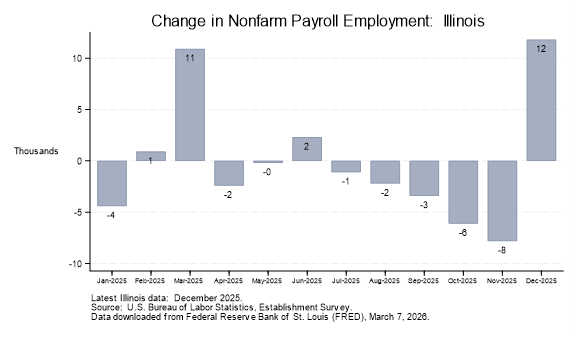

Diving into the monthly employment data shows a choppy picture (see below – data available only through December 2025), with four months of increases, eight months of decreases, and a year’s best showing of 12,000 new jobs in December 2025.

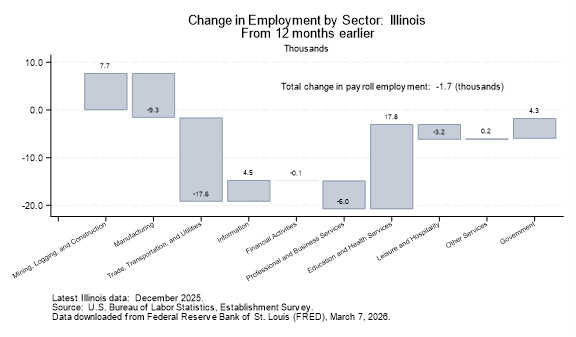

As in the U.S. overall, job growth in Illinois over the past 12 months also relied heavily on strength in the education and health services sector (see chart below). Without that sector’s job gains, employment would have fallen by nearly 20,000 jobs.

Which Sectors Matter Most for Illinois?

Education and Health Services

In 2025, the Education and Health Services sector accounted for 17.3% of nonfarm employment for the U.S. overall but only 16.4% for Illinois, suggesting less local risk from weakness in this sector. However, Illinois’s 2025 job growth was largely due to employment gains in this sector, so this will be a sector to watch as 2026 data becomes available.

Manufacturing

For both Illinois and the nation as a whole, 2025 saw the continuation of the long-term secular decline in factory employment as manufacturers shed jobs. Illinois is somewhat vulnerable to weakness in this sector as manufacturing jobs represent 9.3% of all nonfarm jobs in Illinois (as of 2025) as opposed to 8.0% nationally. Likely factors behind recent job losses are the imposition of aggressive tariffs, the uncertainty around future tariff policies, and the overall economy. Going forward, a sustained increase in oil prices could depress activity and employment in this sector.

Public Sector

Since 2019, growth in public sector employment has been the second largest factor underpinning job growth in Illinois. Government jobs grew by 31,000 between 2019 and 2025, second only to the 72,000 jobs added in the education and health services sector.

Despite losing federal government jobs over the past year, Illinois has seen overall growth in public sector employment, largely due to two factors. First, in 2025, federal government jobs account for a smaller share of public sector employment in Illinois than nationally, 9.4% in 2025 compared to 12.3% nationally. Second, Illinois added 14,000 state and local government roles in 2025, offsetting 2,000 lost federal jobs.

What Should Illinois Expect Next?

As demonstrated by the lack of change over 2024, labor markets appear to be in a bit of a holding pattern at present, with no clear big swings yet evident in the data: job growth is slow, even negative in some sectors, but unemployment rates remain low as labor force growth has stalled. The following are baseline factors that legislators in Springfield must consider as they move ahead with the State’s FY2027 budget.

- Continued policy shocks on tariffs and immigration will likely contribute to overall economic sluggishness over the next few months.

- Recent international hostilities in the Middle East have driven up oil prices, threatening energy-intensive sectors such as transportation and manufacturing, and possibly weakening consumer and business confidence about the future. A sustained increase in oil prices could have a material depressing impact on economic activity, and by extension, cyclically sensitive state tax revenues.

- If weakness in the Education and Health Services sector continues or worsens, that may depress the State’s employment gains going forward.

- The impact of AI on business activity and employment is still far from certain, with conflicting points of view on the speed, intensity, and even direction of AI’s impacts.